Resource Hub

May 18, 2026

| Justin Saeks

Tags: CAR-T manufacturing, CAR-T therapy, Cell and Gene Therapy, Cell therapy, Gene Therapy, In vivo CAR-T

Why Big Pharma is Betting Billions to Fix the CAR-T Manufacturing Problem

For more than a decade, CAR-T cell therapy has represented one of medicine’s most exciting frontiers, a technology capable of sending certain blood cancers into lasting remission after all other treatments have failed. Yet for all its clinical promise, CAR-T has remained frustratingly out of reach for most patients. Rather than scientific, the main reason for this is logistical. That may be about to change, with billions flowing into a new generation of “in vivo” CAR-T companies, signaling that big pharma has resolved to address the problem.

Manufacturing Bottleneck Holding Ex Vivo CAR-T Back

Today’s approved CAR-T therapies, products like Kymriah, Yescarta, and Carvykti, are built on a process known as ex vivo manufacturing. The workflow includes the following steps:

- A patient’s T cells are extracted

- The cells are shipped to a specialized manufacturing facility

- The cells are genetically engineered over several weeks

- The patient receives lymphodepletion chemotherapy to prepare the immune system

- The modified cells are shipped back and infused into the patient

The result is a therapy that is genuinely transformative for the right patient, but costs between $400,000 and $500,000 per treatment, requires four to six weeks of manufacturing time, and is only available at a small number of specialized academic medical centers. For patients with rapidly progressing disease, the wait alone can be fatal.

The manufacturing complexity of ex vivo CAR-T therapies creates a cascade of problems:

- limited production capacity,

- high failure rates for individual patient batches,

- restricted geographic access,

- and extraordinary cost burdens for payers and health systems.

There have been efforts to scale in creative ways, for example through decentralization; however, this has proven difficult. As a result, these challenges present structural limits on how widely CAR-T can scale under the current paradigm.

A Different Approach: Cells Engineered Inside the Body

In vivo CAR-T platforms flip the entire model. Rather than removing cells from a patient, engineering them externally, and then reinfusing them, in vivo CAR-T approaches deliver genetic instructions directly into the body, using specially engineered viral vectors or other mechanisms to reprogram the patient’s T cells in the bloodstream.

The concept and its motivation are simple: if the body can be directed to generate CAR-T cells, then the need for large manufacturing facilities, complex logistics, batch-specific failures, and much of the cost can be reduced. A one-time intravenous infusion could potentially replace a multi-week, multi-institution manufacturing process.

The in vivo CAR-T field has split across two competing delivery platforms, each with a fundamentally different commercial profile. The first approach uses lentiviral (LV) vectors, re-engineered viruses that have had their disease-causing components removed and repurposed as delivery vehicles. Lentiviruses naturally infect a broad range of cell types, so developers have had to solve a targeting challenge: directing them specifically to T cells. This is achieved by modifying the virus’s outer coat protein or swapping it with envelope proteins from related viruses such as Nipah, measles, or Cocal, and then adding antibody-like molecules that recognize T-cell markers such as CD3, CD7, or CD8.

The advantage of this approach is durable expression: once the virus delivers its payload, the CAR is permanently integrated into the T cell genome and can be expressed long term. The drawbacks include potential immune reactions, manufacturing complexity at commercial scale, and a small theoretical risk of unintended genomic insertion.

The second approach uses lipid nanoparticles (LNPs), the same delivery technology used for the Pfizer and Moderna COVID-19 vaccines. LNPs transport mRNA (or more stable circular RNA) encoding the CAR into T cells, where the cell’s own machinery temporarily produces the CAR protein.

This approach offers several advantages: LNPs are less expensive to manufacture at scale using existing infrastructure, and the transient nature of expression allows for repeat dosing if needed. However, these same characteristics introduce trade-offs. LNPs tend to accumulate in the liver rather than efficiently targeting T cells, are less effective than lentiviruses at gene delivery, and produce CAR expression that lasts days to weeks rather than months or years.

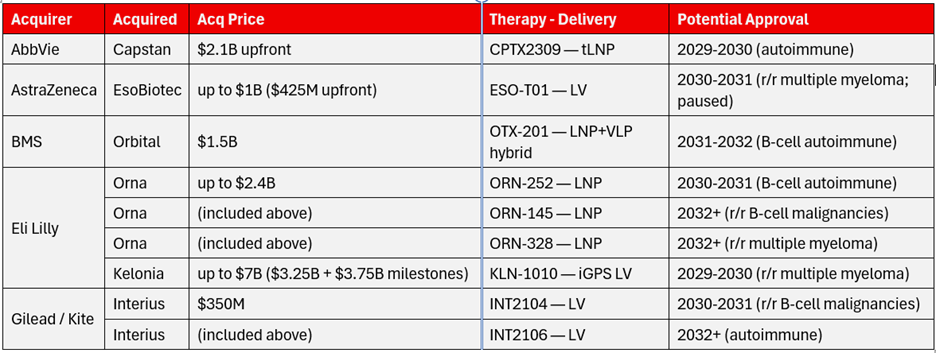

Recent Streak of Acquisitions

Early clinical data, while still limited, has been compelling enough to capture the attention of many of the largest companies in the industry. Examples of major acquisitions in this space over the past year are provided in the following table, which cumulatively account for approximately $15 billion in value.

Lilly’s two deals alone represent nearly $10 billion in committed and contingent capital, a clear statement of conviction from a company that generated $65 billion in revenue in 2025 and is actively diversifying beyond its GLP-1 franchise. What is also notable is not just the size of these deals but their timing, with therapies still in Phase 1 development.

Multiple myeloma and various autoimmune diseases comprise the bulk of the targeted disease areas. As indicated in the fourth column, there is investment in both LV and LNP delivery systems, and the estimated timeframe for regulatory approval begins around 2029, as shown in the right column.

While this activity has increased recently, it may not necessarily represent a sustained trend, as most major immuno-oncology companies now have an in vivo CAR-T position. Notable absences include Novartis and J&J, although J&J’s Janssen division is already active in this market with Carvykti for multiple myeloma. Novartis has stated that it is evaluating the space. A slowdown is likely due to a limited number of remaining viable acquisition targets at the clinical stage. Potential targets that may still attract investment include Umoja Biopharma and Sana Biotechnology. Several Chinese companies are less likely acquisition candidates for Western pharmaceutical firms, including Legend, OriCell, Genocury, and Immorna.

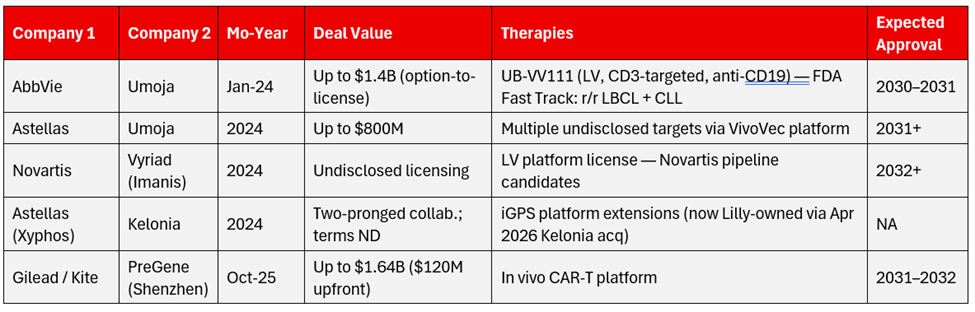

Other Non-Acquisition Deals

There have been several major collaborations and licensing deals in this segment, some of which cover technologies or platforms rather than specific therapies. The following table highlights selected significant deals.

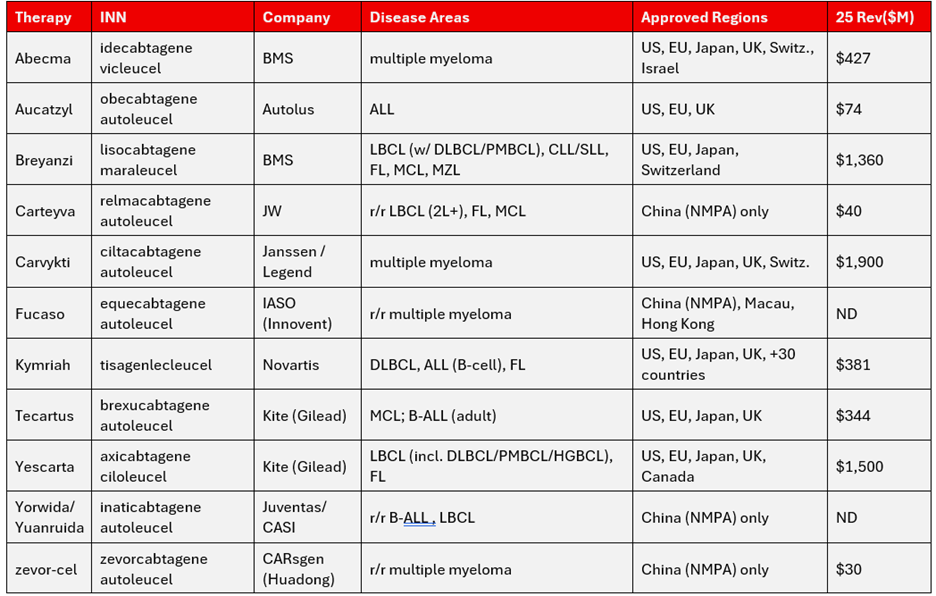

Current Ex Vivo CAR T Products

The current CAR-T landscape spans 12 commercially approved products across two distinct pricing tiers and two distinct regulatory environments. The Western-approved segment, anchored by Carvykti ($1.9 billion), Yescarta ($1.5 billion), and Breyanzi ($1.4 billion), generated roughly $5.5 billion combined in 2025 and continues to be dominated by Gilead’s Kite franchise, BMS, J&J/Legend, and Novartis.

The China-only segment, which partly overlaps and consists of six NMPA-approved products (Akilun, Carteyva, Fucaso, Yorwida, zevor-cel, plus Carvykti’s separately reimbursed Chinese launch), operates at substantially lower price points and contributes a small but rapidly growing share of global CAR-T volume.

B-cell maturation antigen-directed (BCMA-directed) therapies for multiple myeloma, including Abecma, Carvykti, Fucaso, and zevor-cel, represent the highest-revenue indication, while CD19/CD20-directed therapies in r/r LBCL and B-ALL remain the largest by patient volume.

Autolus’s Aucatzyl ($74 million) is the newest Western entrant, launched for adult r/r B-ALL across the U.S., U.K., and EU from late 2024 through mid-2025.

The bar has been raised slightly for new entrants, as the FDA issued guidance in late 2025 that places additional requirements on companies. It is increasingly emphasizing randomized data and comparative evidence. Future CAR-T approvals will likely require randomized controlled trial data with standard-of-care comparators and demonstrated superiority, rather than single-arm trials.

Why Multiple Myeloma Is the Beachhead

It is no coincidence that the leading in vivo CAR-T programs are targeting multiple myeloma. The disease has several characteristics that make it an ideal proving ground for this approach. BCMA is a protein expressed almost universally on malignant myeloma cells and is already validated as a target by approved ex vivo CAR-T therapies such as Carvykti and Abecma.

Kelonia’s KLN-1010 targets BCMA using in vivo lentiviral delivery, and early data have shown signals of deep responses, including MRD negativity in initial patients. From a market standpoint, multiple myeloma represents a large and growing opportunity. It is the second most common blood cancer, with approximately 35,000 new diagnoses per year in the U.S.

Existing ex vivo CAR-T therapies have demonstrated durable responses, establishing clinical proof of concept, but their manufacturing complexity continues to limit broader adoption.

Beyond Oncology: The Autoimmune Wildcard

The long-term strategic significance of in vivo CAR-T extends well beyond oncology. Lilly’s acquisition of Orna Therapeutics was focused on autoimmune disease, a market worth hundreds of billions of dollars globally and one in which existing treatments primarily manage symptoms rather than address underlying immune dysfunction.

The ability to reprogram T cells in vivo to eliminate autoreactive immune cells, which drive conditions such as lupus, rheumatoid arthritis, and inflammatory bowel disease, would represent a fundamentally different category of treatment from those currently available.

Early ex vivo CAR-T data in autoimmune indications have already produced encouraging results in small patient populations, and in vivo delivery could make such approaches broadly accessible for the first time. This helps explain why companies such as Lilly are committing substantial capital. These investments extend beyond oncology pipelines, reflecting interest in platform technologies with applications across multiple therapeutic areas.

Potential Effects on the Market

This anticipated wave of in vivo CAR-T therapies may represent an inflection point rather than a gradual evolution of the pipeline. The resulting changes could therefore be more pronounced. Several dynamics are likely to be important to monitor:

- Competitive consolidation: The number of viable targets has been shrinking, and remaining players may attract premium valuations

- Manufacturing disruption: Reduced demand is expected for ex vivo cell therapy manufacturing, alongside increased demand for viral vector production, process development, and gene delivery characterization tools

- Reimbursement and access implications: Lower costs and simplified administration could expand access beyond specialized centers

- Regulatory development: Competitive dynamics and timelines will be shaped in part by evolving FDA and international regulatory frameworks for evaluating these therapies