Store

In Vitro Diagnostics (IVD) in the United States: Comprehensive Market Overview 2024-2029

Publication Date: November 25, 2024

Tags: Coagulation, COVID-19, Diagnostic Instruments, Genetic Diseases, Hematology, Histology and Cytology, Immunoassay, In Vitro Diagnostics (IVD), Infectious Diseases, Molecular Diagnostics, Oncology and Cancer, Point-of-Care (POC) Testing, US and Canada

Pages: 210

SKU: 24-031

The U.S. in vitro diagnostics (IVD) market remains the largest and most influential in the world. This multi-billion-dollar industry serves as the incubator for cutting-edge medical technologies, driving innovation and setting the benchmark for diagnostic standards worldwide. Yet, this dynamic market faces a period of transformation, balancing challenges such as cost pressures, regulatory changes, and the lingering impacts of COVID-19—all while adapting to a rapidly aging population and increasing demand for precision diagnostics.

Kalorama Information’s latest report, In Vitro Diagnostics (IVD) in the United States: Comprehensive Market Overview 2024-2029, delivers a comprehensive analysis of the trends, technologies, and players driving this critical sector. With data-backed insights, this report is your definitive guide to understanding the complexities of the U.S. IVD market.

The U.S. IVD market is a cornerstone of global healthcare innovation—but it is also a market in transition In Vitro Diagnostics (IVD) in the United States: Comprehensive Market Overview 2024-2029, the fifth edition in Kalorama’s ongoing series, offers unparalleled access to insights on the trends and technologies that will define the industry’s future.

This Report is Essential for:

- Identifying market gaps and opportunities for product innovation.

- Gaining a competitive edge with strategic insights into the U.S. diagnostic landscape.

- Making informed decisions by understanding market dynamics and future potential.

- Staying updated on how evolving regulations are shaping the IVD market.

What’s in the Report:

- Comprehensive Market Analysis: Gain detailed insights into key U.S. IVD segments, including:

- Clinical Chemistry

- Microbiology (Traditional) – Identification and Antibiotic Susceptibility Testing (ID/AST)

- Microbiology – Molecular- Infectious Disease

- Point-of-Care (POC) Tests – Diabetes

- Point-of-Care (POC) Tests – All Other

- Immunoassays – Infectious Disease (non-POC)

- Immunoassays – Other

- Molecular – Non-infectious Disease

- Hematology

- Coagulation (non-POC)

- Histology

- Blood Testing and Typing

- Others

- Stay Ahead of the Curve: Understand how demographic shifts, technological advancements, and public health challenges are reshaping the market.

- Competitive Intelligence: Explore profiles of leading IVD companies, such as Roche Diagnostics, Abbott, Siemens Healthineers, and Thermo Fisher Scientific, and stay informed about their latest developments.

- Data-Driven Insights: With market data spanning 2024–2029, this report equips readers with the knowledge to identify growth opportunities and make informed decisions.

Report Highlights:

- Extensive Market Coverage: Dive deep into U.S. IVD segments, from microbiology and hematology to histology and blood typing.

- Top Company Profiles: Learn about the strategies and innovations of 20+ key players, including emerging trends and M&A activities.

- Actionable Insights: Leverage the report’s findings to assess the current standard of care, forecast future trends, and anticipate market penetration for new tests and technologies.

For further details and to purchase directly, please contact us.

Table of Contents

Chapter 1: Executive Summary

U.S. IVD Market

- Table 1-1: U.S. IVD Market by Segment 2024-2029 ($ million) (Blood Typing, Clinical Chemistry, Coagulation, Hematology, Histology, Immunoassay [Immunoassay Infectious Disease, Immunoassay non-Infectious], Microbiology – ID/AST, Molecular [Molecular Infectious Disease with NAT & mass spec, Molecular – non-Infectious Disease], POC – Other, POC Diabetes [all], Others)

- Figure 1-1: U.S. IVD Market Segments by % of the Total U.S. IVD Market, 2024 (Blood Typing, Clinical Chemistry, Coagulation, Hematology, Histology, Immunoassay [Immunoassay Infectious Disease, Immunoassay non-Infectious], Microbiology – ID/AST, Molecular [Molecular Infectious Disease with NAT & Mass Spec, Molecular – non-Infectious Disease], POC – Other, POC Diabetes [all], Others)

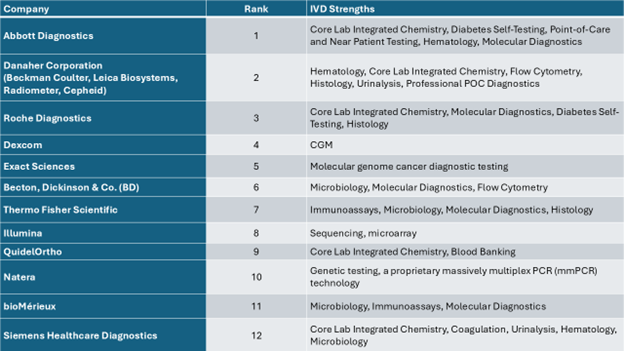

Top 12 U.S. IVD Market Participants and Rankings

- Table 1-2: U.S. IVD Market Rankings by Estimated 2024 US Revenue – Top 12 Companies (Abbott Diagnostics, Becton, Dickinson & Co. [BD], bioMérieux, Danaher Corporation [Beckman Coulter, Leica Biosystems, Radiometer, Cepheid], Dexcom, Exact Sciences, Illumina, Natera, QuidelOrtho, Roche Diagnostics, Siemens Healthcare Diagnostics, Thermo Fisher Scientific)

Scope and Methodology

Conclusions

Chapter 2: Introduction to U.S. Health Care

The United States and In Vitro Diagnostics

U.S. Patient Population

Healthcare System Utilization

Aging

- Figure 2-1: U.S. Projects of Older Adult Population, 2016-2060 (million)

Disease Prevalence and Incidence

- Table 2-1: U.S. Cancer Cases, Estimates 2024

- Table 2-2: Reported Cases of Selected Notifiable Diseases, U.S., 2022

U.S. Clinical Lab Expenditure

- Table 2-3: U.S. Clinical Lab Market, by Channel, 2023 (% of Market)

Preventive Health Care

Product Innovation from Value-Based Pricing

Clinical Testing under Medicare – Reimbursement Cuts and Market-Based Pricing

Protecting Access to Medicare Act of 2014 (PAMA)

- Table 2-4: Implemented and Proposed Clinical Diagnostic Laboratory Test Rates, 2020-2027

Impact of CARES Act on PAMA

Saving Access to Laboratory Service Act (SALSA)

Advanced Laboratory Tests (ADLT)

- Table 2-5: List of Approved ADLTs, March 2024

Personalized Medicine

Companion Diagnostics

- Table 2-6: FDA Approved Companion Cancer Diagnostics, 2024

AI Use in U.S. Liquid Biopsy Segment

- Table 2-7: Selected S. AI/Liquid Biopsy Initiatives

Telehealth

Laboratory-Developed Tests (LDTs)

FDA

U.S. Healthcare Infrastructure and Testing Channels

Hospitals

Independent Labs

Physician Office Laboratories

At-Home Testing

Home Collection Trend

- Table 2-8: Home Collection Test Kit Market, by Category, Worldwide, 2022 (% Estimated Share) (Cholesterol, Drug of Abuse, Fertility Testing, Genetic, Infectious Disease [COVID-19, STDs, HIV, etc.], Tumor DNA Markers, Other [Hormone, Allergies, HbA1c, Heavy Metals, etc.])

- Table 2-9: Selected Molecular Tests EUAs for Home Collection SARS-CoV-2 Tests, 2020-2024

Retail Clinics

Conclusions

Chapter 3: U.S. IVD Market Analysis

Clinical Chemistry

- Table 3-1: U.S. Clinical Chemistry Market, by Segment, 2024-2029 ($ million) (Blood Gases, General Chemistry, Urinalysis)

- Figure 3-1: U.S. Clinical Chemistry Market, 2024-2029 ($ million)

Microbiology and Virology – ID/AST and Molecular

- Table 3-2: US ID/AST Microbiology ID/AST Market, by Segment, 2024-2029 ($ million) (Auto ID/AST, Manual ID/AST, Blood Culture, Chromogenic Media, Rapid, Micro)

- Figure 3-2: U.S. ID/AST Microbiology Market, 2024-2029 ($ million)

Molecular Infectious Disease

- Table 3-3: U.S. Molecular Infectious Disease, Market Distribution Estimates by Segment, 2024 (%) (HAI/Sepsis, HIV, Hepatitis, GC/Chlamydia, Respiratory, Mycobacteria/TB, Other Microbiology)

- Figure 3-3: U.S. Molecular Microbiology/Virology Market Distribution Estimates, by Segment, 2024 (%) (HAI/Sepsis, HIV, Hepatitis, GC/Chlamydia, Respiratory, Mycobacteria/TB, Other Microbiology)

Point-of-Care Testing

- Table 3-4: U.S. Point-of-Care (POC) Diagnostics Markets by Segment, 2024-2029 ($ million) (Glucose, Blood & Electrolytes, Coagulation, Cardiac Markers, Drugs of Abuse, Pregnancy & Fertility, Fecal Occult Blood, Infectious Disease, Lipid, Cancer Tumor Markers, Urine, Miscellaneous)

- Figure 3-4: U.S. POC Diabetes Market, 2024-2029 ($ million)

- Figure 3-5: U.S. POC Market without Diabetes, 2024-2029 ($ million)

Immunoassays

Non-Infectious Disease Immunoassay

- Table 3-5: U.S. Immunoassays Market – Non Infectious, by Segment, 2024-2029 ($ million) (Cardiac Markers, Tumor Markers, Autoimmune, Allergy, Thyroid, Proteins, Anemia, Fertility, Therapeutic Drugs, Vitamin D, HbA1c, Others)

- Figure 3-6: U.S. Immunoassays Market – Non Infectious, 2024-2029 ($ million)

Infectious Disease Immunoassay

- Table 3-6: U.S. Immunoassays Market – Infectious, 2024-2029 ($ million) (Hepatitis, HIV, STDs, ToRCH, Respiratory, HAIs/Sepsis, Others)

- Figure 3-7: U.S. Immunoassay Infectious Disease, 2024-2029 ($ million)

Molecular Non-Infectious Disease Diagnostics

- Figure 3-8: U.S. Molecular – Non-Infectious Disease Diagnostics Market, 2024-2029 ($ million)

Coagulation

- Table 3-7: U.S. Coagulation Diagnostics Market, by Segment, 2024-2029 ($ million) (PT/INR, Molecular-lab Thrombophilia SNPs, D-Dimer)

- Figure 3-9: U.S. Coagulation Diagnostics Market, 2024-2029 ($ million)

Histology

- Table 3-8: U.S. Histology/Cytology IVD Market, by Segment, 2024-2029 ($ million) Pap Tests, in situ Hybridization, Immunohistochemistry, Traditional non-Pap Stains, HPV Molecular)

- Figure 3-10: U.S. Histology and Cytology Diagnostics Market, 2024-2029 ($ million)

Hematology

- Table 3-9: U.S. Lab-based Hematology Market, by Analyte 2024-2029 ($ million)

- Figure 3-11: U.S. Hematology Diagnostics Market, 2024-2029 ($ million)

Blood Testing and Typing

- Table 3-10: U.S. Blood Testing and Typing, by Segment, 2024-2029 ($ million) (ABO Grouping/Typing, Screening)

- Figure 3-12: U.S. Blood Grouping and Typing Diagnostics Market, 2024-2029 ($ million)

- Figure 3-13: U.S. Blood Screening Diagnostics Market, 2024-2029 ($ million)

Total U.S. IVD Market

- Table 3-11: U.S. IVD Market by Segment 2024-2029 ($ million) (Blood Typing, Clinical Chemistry, Coagulation, Hematology, Histology, Immunoassay [Immunoassay Infectious Disease, Immunoassay non-Infectious], Microbiology – ID/AST, Molecular [Molecular Infectious Disease with NAT & mass spec, Molecular – non-Infectious Disease], POC – Other, POC Diabetes [all], Others)

- Figure 3-14: U.S. IVD Market Segments by % of the Total U.S. IVD Market, 2024 (Blood Typing, Clinical Chemistry, Coagulation, Hematology, Histology, Immunoassay [Immunoassay Infectious Disease, Immunoassay non-Infectious], Microbiology – ID/AST, Molecular [Molecular Infectious Disease with NAT & Mass Spec, Molecular – non-Infectious Disease], POC – Other, POC Diabetes [all], Others)

Chapter 4: Competitor U.S. IVD Market Players

- Table 4-1: Top 12 U.S. IVD Competitor Revenues, 2024 ($ million) (Abbott Diagnostics, Becton, Dickinson & Co. [BD], bioMérieux, Danaher Corporation [Beckman Coulter, Leica Biosystems, Radiometer, Cepheid], Dexcom, Exact Sciences, Illumina, Natera, QuidelOrtho, Roche Diagnostics, Siemens Healthcare Diagnostics, Thermo Fisher Scientific)

Abbott Diagnostics

Abbott Diagnostic Recent Revenue History

- Table 4-2: Global Abbott Diagnostics (and Diabetes Management) Revenues, 2019-2023 ($ million)

- Figure 4-1: Abbott Diagnostics – IVD U.S. Revenues vs Non U.S. IVD Revenues, 2023 ($ million)

- Table 4-3: Global Abbott Diagnostics Revenues, 2019-2023 ($ million)

Core Lab

Hematology

Blood Banking

Infectious Diseases – Molecular

Diabetes

HIV Point of Care

i-STAT Business

Becton, Dickinson and Company (BD)

Recent Revenue History

- Table 4-4: Global BD Life Sciences Revenues, 2019-2023 ($ million)

- Figure 4-2: BD – IVD U.S. Revenues vs Non U.S. IVD Revenues, 2023 ($ million)

Cytology

Molecular Microbiology

Traditional Microbiology – ID/AST

Blood Culture

Hospital Acquired Infections

Blood Collection

Mass Spectrometry

Flow Cytometry

bioMérieux

- Table 4-5: Global bioMérieux IVD Revenues, 2019-2023 ($ million)

- Figure 4-3: bioMérieux – IVD U.S. Revenues vs Non U.S. IVD Revenues, 2023 ($ million)

- Table 4-6: Global bioMérieux Revenues in Selected Test Segments, 2019-2023 ($ million)

Traditional Microbiology

Immunoassays

BIOFIRE Diagnostics Business

Danaher Corporation

Recent Revenue History

- Table 4-7: Global Danaher Diagnostics Revenues, 2019-2023 ($ million)

- Figure 4-4: Danaher – IVD Diagnostic U.S. Revenues vs Non U.S. IVD Revenues, 2023 ($ million)

Beckman Coulter

Cepheid

Dexcom

- Table 4-8: Global Dexcom Revenue History 2019-2023 ($ million)

- Figure 4-5: Dexcom – IVD Diagnostic U.S. Revenues vs Non U.S. IVD Revenues, 2023 ($ million)

Exact Sciences

Recent Revenue History

- Table 4-9: Global Exact Sciences Revenue History, 2019-2023 ($ million)

- Figure 4-6: Exact Sciences – IVD Diagnostic U.S. Revenues vs Non U.S. IVD Revenues, 2023 ($ million)

Hologic, Inc.

Recent Revenue History

- Table 4-10: Hologic Revenues, 2019-2023 ($ million)

- Figure 4-7: Hologic – IVD Diagnostic U.S. Revenues vs Non U.S. IVD Revenues, 2023 ($ million)

- Table 4-11: Global Hologic Revenues in Selected Test Segments, 2019-2023 ($ million) estimated

Panther Molecular System

Panther Fusion

Infectious Diseases

Sexually Transmitted Infections

Cytology

Illumina

- Table 4-12: Global Illumina Revenue History, 2019-2023 ($ million – not all revenues are for clinical products and services; estimated)

- Figure 4-8: IVD Diagnostic U.S. Revenues vs Non U.S. IVD Revenues, 2023 ($ million) estimated

- Table 4-13: Global Illumina Diagnostic Revenues, by Segment, 2019-2023 ($ million) estimated

Natera

Recent Revenue History

- Table 4-14: Natera Revenue History, 2019-2023 ($ million)

- Figure 4-9: Natera – IVD Diagnostic U.S. Revenues vs Non U.S. IVD Revenues, 2023 ($ million) estimated

QuidelOrtho Corporation

- Table 4-15: Global QuidelOrtho Revenue History, 2019-2023 ($ million)

- Figure 4-10: QuidelOrtho – IVD Diagnostic U.S. Revenues vs Non U.S. IVD Revenues, 2023 ($ million) estimated

- Table 4-16: Global QuidelOrtho Diagnostic Revenues, by Segment, 2020-2023 ($ million) estimated

Immunoassays

Rapid Immunoassays

The Solana Business

Molecular – Savanna

Blood Bank

Roche Diagnostics

Recent Revenue History

- Table 4-17: Global Roche IVD Diagnostics Revenues, 2019-2023 ($ million)

- Figure 4-11: Roche – IVD Diagnostic U.S. Revenues vs Non U.S. IVD Revenues, 2023 ($ million) estimated

- Table 4-18: Global Roche IVD Diagnostics Revenues, by Type, 2019-2023 (million) estimated

Immunoassays

Core Molecular

Digital PCR

Diabetes Care

cobas Liat System – POC

HPV

Blood Bank

Cancer Companion Testing

Siemens Healthineers (Siemens)

Recent Revenue History

- Table 4-19: Global Siemens Healthineers IVD Revenues, 2019-2023 ($ million)

- Figure 4-12: Siemens Healthineers – IVD Diagnostic U.S. Revenues vs Non U.S. IVD Revenues, 2023 ($ million)

- Table 4-20: Global Siemens Healthineers Diagnostic Revenues, by Segment, 2021-2023 ($ million) estimated

Core Lab

Immunoassays

Hematology

Molecular

Thermo Fisher Scientific Inc.

Recent Revenue History

- Table 4-21: Global Thermo Fisher IVD Revenues, 2019-2023 ($ million)

- Figure 4-13: Thermo Fisher – IVD Diagnostic U.S. Revenues vs Non U.S. IVD Revenues, 2023 ($ million)

- Table 4-22: Global Thermo Fisher IVD Revenues, by Type, 2019-2023 (million) estimated

Immunoassays

Microbiology

Molecular Test Business

Next Generation Sequencing

qPCR

Oncology Companion Diagnostics

Mass Spectrometry

Related products

In Vitro Diagnostic (IVD) Trends and Market Update, 2025

December 2, 2025

Updated December 2025

Kalorama Information’s In Vitro Diagnostic (IVD) Trends and Market Update, 2025 delivers critical insights into the evolving IVD market amid global economic uncertainties. Published twice annually—in April and in December following the release of Kalorama’s flagship study, The Worldwide Market for In Vitro Diagnostics (IVD), 18th Edition—this report serves as both a standalone resource and…

Price range: $5,600.00 through $8,000.00

30-Country In Vitro Diagnostic (IVD) Market Atlas, 2025

December 19, 2025

Updated December 2025

Kalorama Information’s 30-Country IVD Market Atlas, 2025 provides a comprehensive analysis of the in vitro diagnostic (IVD) markets across 30 key countries, including the U.S., China, Germany, UK, Saudi Arabia, India, UAE, France, Vietnam, and Turkey, among others. This in-depth report delivers detailed market sizing, forecasts for 2029 and 2030,…

Price range: $5,600.00 through $8,000.00

IVD Test Procedure Volumes, 2024-2029

October 8, 2024

Kalorama Information’s IVD Test Procedure Volumes, 2024-2029 report provides a deep dive into the global trends shaping in vitro diagnostic (IVD) procedural volumes. Designed to complement Kalorama’s comprehensive market analysis in The Worldwide Market for In Vitro Diagnostic (IVD) Tests, 17th Edition, this essential report delivers actionable data on the growth, challenges, and emerging opportunities…

Price range: $6,300.00 through $9,450.00